In this commentary, CFW Associate Dr Anis Chowdhury explains why a lower unemployment rate, on its own, is not a solution to Australia’s labour market and social challenges.

Don’t Be Fooled: A Lower Unemployment Rate is Not a Magic Bullet

Two days before the federal election, comes news that Australia’s unemployment rate had slipped below 4% in March, to 3.9% – the lowest rate in 48 years.

But this aggregate number hides some hard realities for struggling vulnerable people. For example, the youth unemployment rate increased to 8.8%. About 3 million Australian workers lack basic job security. That includes some 2.4 million workers in casual positions, with no paid leave entitlements. A further 500,000 are on fixed-term contracts. A survey by PwC found that anxiety about the economic future intensified due to the pandemic. Some 56% of Australians now believe few people will have stable, long-term employment in the future (more than two years).

Meanwhile, the labour force participation rate decreased to 66.3% in March as workers continue to suffer from the pandemic’s scars – including mental health challenges and long COVID’s debilitating health issues. So this apparent labour market tightening is misleading: it is mainly due to this decline in the participation rate, as well as pandemic restrictions on migrant workers (including students and seasonal travellers) which have sharply constrained the size of Australia’s labour force.

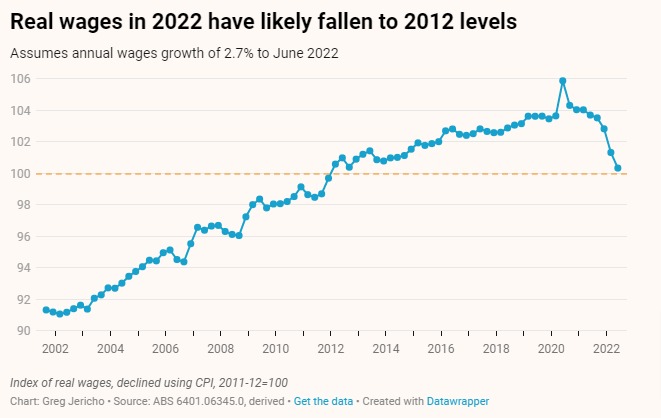

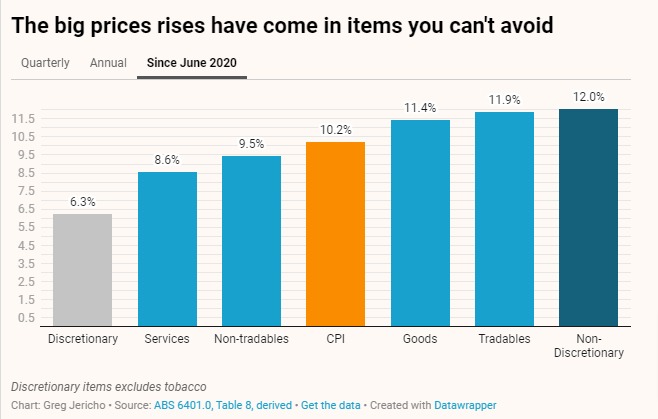

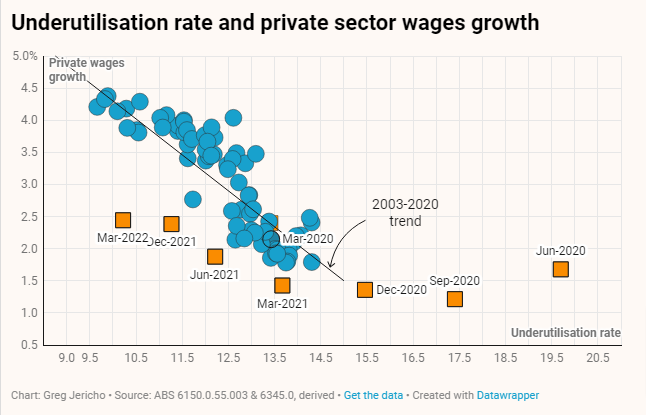

Most telling, Australia’s recent falling unemployment rate is having little effect on wages growth; wages grew 2.4% in the year to March, up only marginally on the 2.3% from the previous reading; and less than half the 5.1% rate of inflation.

Rising interest rates will now deliver a further blow to the living conditions of ordinary citizens as they struggle to service their debts. With household debt equal to about 120% of annual GDP, Australian households are among the most indebted in the world. As the Reserve Bank is poised to raise interest rates further, Andrew McKellar of the Australian Chamber of Commerce has warned that Australians “have to be very careful”; interest rate hikes are “set to affect Australian businesses nationwide across a number of sectors”.

So it’s not being alarmist to warn that a recession could be just around the corner: one that would see unemployment rising alongside inflation. The Reserve Bank has little control over the factors (mainly global supply chain disruptions, and rising food and fuel prices) that have led the current cost-of-living inflation. Past history suggests that central banks’ efforts to disinflate the economy produce slower growth, higher unemployment, and often recessions.

Address the deeper malaises

No matter who wins the current federal election, the incoming government will have to tackle deeper malaises in the Australian economy. They include stagnating productivity growth and the falling labour income share in GDP.

Australia’s aggregate labour productivity growth (real output per hour) has stayed mainly in a band between 1.2 and 2.5% per year during the last 50 years; it fell to 0.2% during 2018-2019, but has rebounded since the pandemic (averaging 2% per year from end-2019 through end-2021). Productivity growth is a key source of long term economic and income growth, and as such, is an important determinant of a country’s average living standards. Productivity gains also drive down the cost of goods and services and enhance international competitiveness.

The impact of productivity growth on standards of living has been undermined, however, by capital’s capture of productivity gains. Real wages have grown much more slowly than real labour productivity (and now, with surging inflation, real wages are falling rapidly). Thus, labour income’s share in Australia steadily declined from the peak of around 58.5% in the mid-1970s to a record low of 46% of GDP at end-2021, as the gap between productivity growth and real wage growth widened.

Among many factors, wage-suppressing policies and increased job insecurity have contributed to this dismal outcome. More than half of Australian participants in the PwC survey (61%) felt the government should act to protect jobs, with that opinion more acute among 18-34 year-olds (63%) than those over 65 (50%).

Both the Reserve Bank of Australia and Treasury have made clear, Australia’s low wage growth is a major drag on the economy. But low wage growth was not accidental; the former Coalition Finance Minister, Matthias Cormann, now OECD Secretary-General, described (downward) flexibility in the rate of wage growth as “a deliberate design feature of our economic architecture”.

Looking after workers is good economic policy

Coalition leaders attacked Labor leader Albanese’s support for raising the minimum wage, claiming without evidence that a big increase in the minimum wage might force some workplaces to close. The business lobbies also joined the chorus.

But is this opposition to higher wages grounded in good economics? The available historical evidence, as well as theoretical considerations, say: “no”.

Robert Bosch, the German industrialist, engineer and inventor, founder of Robert Bosch GmbH (electrical co), introduced 8-hour working days in 1906, free Saturdays in 1910, and other benefits for his workers. He said: “I don’t pay good wages because I have a lot of money; I have a lot of money because I pay good wages.”

Henry Ford, the American industrialist, the founder of the Ford Motor Company, and developer of the assembly line, doubled the pay of his workers to $5 a day in 1914. In justifying his decision he said: “Of course the higher wage drew a more productive worker. But that wasn’t the real reason. The fact was, it was no good mass-producing a cheap automobile if there weren’t masses of workers and farmers who could afford to buy it.”

Both Bosch and Ford realised that better pay and working conditions attract better workers and raise their productivity. They also knew that better pay and working conditions also lead to higher sales and revenues. Therefore, overall profit rises despite a higher labour cost. It is no wonder that both their companies not only survived but also became leading global companies.

Singapore, which began its industrialisation by initially taking advantage of cheap labour, has used a deliberate high-wage policy since the early 1980s to move toward high value-added activities. It thus maintained its dynamism not by cutting wages and working conditions, but by incentivising companies (in part through higher wages) to upgrade skills and technology, and hence improve productivity.

In other words, regular upward adjustment of wages can be an effective industry policy tool for accelerating innovation, upgrading, and productivity. Hence, higher wages and better working conditions do not necessarily cause loss of competitiveness in the international market.

Industry-wide bargaining can boost productivity and real wages

More than half a century ago two leading Australian academics – WEG Salter and Eric Russel – argued for tying wage increases in any industry to productivity trends across the whole industry, through a system of industry-wide bargaining. By adhering to industry-wide average productivity-based wage increases, they argued, industry bargaining raises relative unit labour costs of firms with below-industry-average productivity, thereby forcing them to improve their productivity or else exit the industry. At the same time, firms with above-industry-average productivity enjoy lower unit labour costs, hence higher profit rates for reinvestment – favouring the growth of more efficient firms. As mentioned earlier, Singapore used this approach to restructure its industry in the 1980s towards higher value-added activities, with great success.

In contrast, trying to compete on the basis of low wages is a recipe for failure. Low-wage countries typically demonstrate lower productivity; and research by a leading French economist, Edmond Malinvaud, showed that a reduction in wage rates has a depressing effect on capital intensity.

Salter’s research implies that the availability of a growing pool of low paid workers makes firms complacent with regard to innovation and technological or skill upgrading. Under-paid labour provides a way for inefficient producers and obsolete technologies to survive. Firms become caught in a low-level productivity trap from which they have little incentive to escape – a form of ‘Gresham’s Law,’ whereby bad labour standards drive out good. The discipline imposed on all firms as a result of negotiated industry-wide wage increases forces all of them to innovate and become more efficient.

Need wide-ranging policy shifts

Of course, industry-wide bargaining alone cannot solve all the problems of wage inequity or wage stagnation. It must be part of a broader suite of policy measures, to provide all-round support for greater equality and inclusive prosperity.

For example, the next government should also address the system that produces sky-rocketing executive pay at the expense of workers. The annual CEO pay survey shows a drastic jump of an average of 24% during the pandemic, with annual bonuses soaring by 67% – the highest increase in recent record, while workers are suffering real income losses.

A lower marginal tax rate is one of the incentives for the executives to pay themselves heftily, but tax cuts are not found to boost growth or employment. Share options for CEOs, which encourage job cuts and discourage re-investment, also must be reined in.

If anything is making the Australian economy vulnerable, it is the growing economic disparity between self-serving executive compensation and stagnant wages for the rest of the population.

The post Unemployment Rate Does Not Tell the Whole Story appeared first on The Australia Institute's Centre for Future Work.