Today’s 5.75% award wage increase is a necessary boost for the lowest paid workers but does not keep pace with inflation.

The Fair Work Commission (FWC) has today explicitly said this increase “will consequently not cause or contribute to any ‘wage price spiral’”.

Key Points:

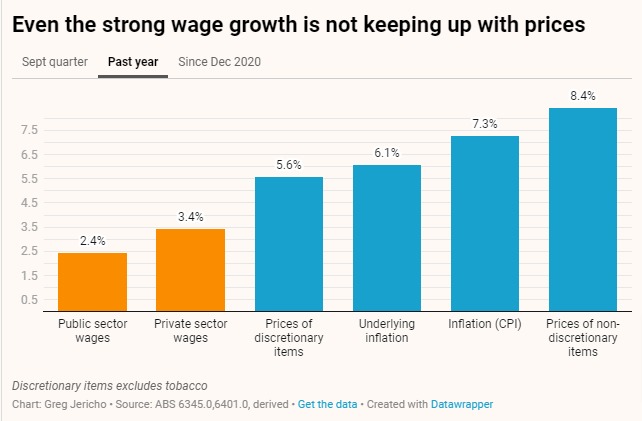

- Award wage increase of 5.75% is less than inflation, which is running at 7%. (This covers approx. 20% of workers)

- FWC Commission have said explicitly this will not cause or contribute to a so-called ‘wage-price spiral’

- FWC acknowledges the increase “will not maintain the real value of modern award minimum wages nor reverse the reduction in real value which has occurred”

- Australia Institute research shows excess corporate profits, not wages, are the major driver of inflation

- Fair Work Commission also increased the national minimum wage by 8.65% (this covers approx 0.7% of workers)

“This is a necessary boost, but insufficient to keep the lowest paid workers ahead of inflation,” said Dr. Greg Jericho, Policy Director at the Australia Institute’s Centre for Future Work.

“It’s significant that the Fair Work Commission has explicitly said this will “not cause or contribute to any wage-price spiral”. At a time when companies are making record profits, our research shows profits, not wages, are the major driver of inflation.

“The FWC notes it “will make only a modest contribution to total wages growth in 2023-24 and will consequently not cause or contribute to any wage-price spiral.

“The FWC has made it clear the Reserve Bank can not blame low paid workers wages for driving inflation in the event they raise interest rates next week.”

Excerpt from Fair Work Commission Decision:

As the total wages of modern award-reliant workers constitute a limited proportion of the national wage bill, we are confident that the increase we have determined will make only a modest contribution to total wages growth in 2023-24 and will consequently not cause or contribute to any wage-price spiral.

We acknowledge that this increase will not maintain the real value of modern award minimum wages nor reverse the reduction in real value which has occurred over recent years.

The post Fair Work: 5.75% Award Wage Boost will not cause “Wage-Price Spiral” appeared first on The Australia Institute's Centre for Future Work.