The dramatic expansion of business profits has gone mostly ignored by the RBA and other macroeconomic policy-makers, who have focused instead on a supposed ‘wage-price’ spiral which does not exist. This suggests the focus of the RBA on wage restraint is misplaced and unfair, and that interest rates would be far lower today if companies had not gouged customers at the checkout.

The report Profit-Price Spiral: The Truth Behind Australia’s Inflation (attached) comes in the same week supermarket giants Woolworths and Coles posted soaring profits, with banks, gas and petrol companies posting similarly soaring returns.

Key Findings:

- A Profit-Price spiral is the main driver of inflation in Australia, rather than a supposed “Wage-Price” spiral, which does not exist

- As of the September quarter of 2022 (most recent data available), Australian businesses increased prices by a total of $160 billion per year over and above their higher expenses for labour, taxes, and other inputs, and over and above profits generated by growth in real economic output

- Without the inclusion of those excess profits in final prices for Australian-made goods and services, inflation since the pandemic would have been much slower: an annual average of 2.7% per year, barely half of the 5.2% annual average actually recorded since end-2019.

- That pace of inflation would have fallen within the RBA’s target inflation band (equal to its 2.5% target, plus-or-minus 0.5%)

- Excess corporate profits account for 69% of additional inflation beyond the RBA’s target. Rising unit labour costs account for just 18% of that inflation

- The RBAs 9 back-to-back interest rate rises would have been unlikely without excess profits and prices based on the RBA’s own policy framework

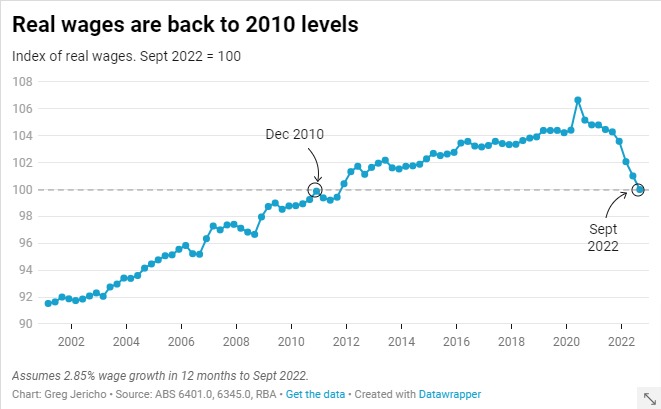

- Real wages in Australia fell 4.5% in 2022, the largest fall on record

“This empirical evidence shows excess corporate profits are the main culprit driving inflation, not workers’ wages,” said Dr. Jim Stanford from the Australia Institute’s Centre for Future Work.

“For Australians doing it tough this data would be aggravating.

“We’ve been told a story that workers need to restrict wage growth and accept a permanent reduction in living standards in order to fix inflation. This evidence shows that’s an economic fairytale.

“ABS data shows that without excess price hikes through the pandemic, inflation would likely be within the RBA target band, and hence there would be no need for the nine extreme, back-to-back interest rate rises that are crushing households and mortgage holders, fuelling the cost-of-living crisis.

“The pain experienced by workers through current inflation contrasts sharply with unprecedented increases in business profitability at the same time.

“Through this episode of post-COVID inflation, real wages have declined rapidly, labour’s share of GDP has declined, and corporate profits have set records. That is completely opposite from the experience of the 1970s, when real wages rose, labour’s share of GDP increased, and corporate profit margins fell.

“History confirms that fears of a 1970s-style ‘wage price spiral’ are simply not justified or grounded in reality. Instead, inflation in Australia since the pandemic clearly reflects a profit-price dynamic.”

The new report ‘Profit-Price Spiral: The Truth Behind Australia’s Inflation’ is attached and comes from the Australia Institute’s Centre for Future Work, by Dr. Jim Stanford.

Supermarkets, banks and petrol companies have recently posted huge profits:

- On Thursday Qantas posted $1.4b half-year profits, tripling revenues

- On Wednesday Woolworths posted a 25% rise in profits. Supermarket profits have soared on the strength of rapid food price inflation.

- On Tuesday Coles net profit grew 11% in the latest half-year result announced Monday, beating forecasts.

- On Wednesday Santos posted a 221% annual profit

- Ampol, Australia’s largest oil refiner, reported a 30% increase in first-half net profit, buoyed by soaring petrol prices.

- Commonwealth Bank posted a record $5.1b billion profit, up 9%, buoyed by extra interest income from rising interest rates.

The post Profit-Price Spiral: Excess Profits Fuelling Inflation & Interest Rates, not Wages appeared first on The Australia Institute's Centre for Future Work.