Read the full article Real wages are shrinking, these figures put it beyond doubt on The Conversation.

The post Real wages are shrinking, these figures put it beyond doubt appeared first on The Australia Institute's Centre for Future Work.

Read the full article Real wages are shrinking, these figures put it beyond doubt on The Conversation.

The post Real wages are shrinking, these figures put it beyond doubt appeared first on The Australia Institute's Centre for Future Work.

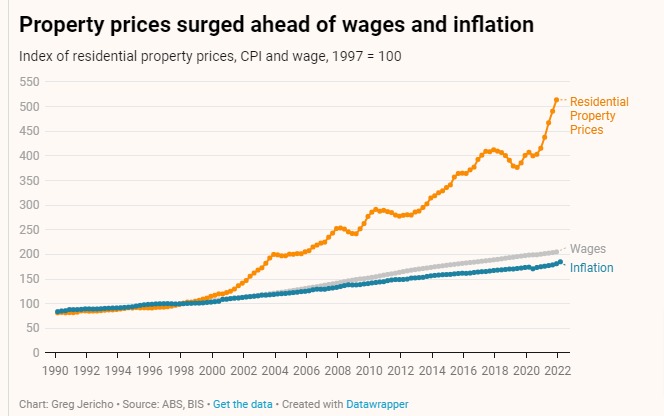

The problem is that for many decades, housing policies have overwhelmingly been geared toward increasing demand within the private-sector housing market. This has only served to pump prices and make it harder for first-home buyers to enter the market, and also increasing the age that people are buying their first home.

Policy Director, Greg Jericho, writes in a column for Guardian Australia, that we need to instead focus on the supply side – increasing the stock of housing – and we also need to be bold enough to look outside the typical private-sector model.

The Australia Institute’s Nordic Policy Centre has proposed a number of measures that have been pursued in Norway, Sweden and Finland that show the solution to housing affordability is not about creating tax distortions that benefit homeowners or which serve only to transfer money from low-income people to the wealthy, but instead treats housing as a need rather than just a wealth-building asset.

After decades of failure, the solution to housing affordability needs to be something other than more policies designed to lift housing prices.

The post To really address housing affordability we need to think differently appeared first on The Australia Institute's Centre for Future Work.

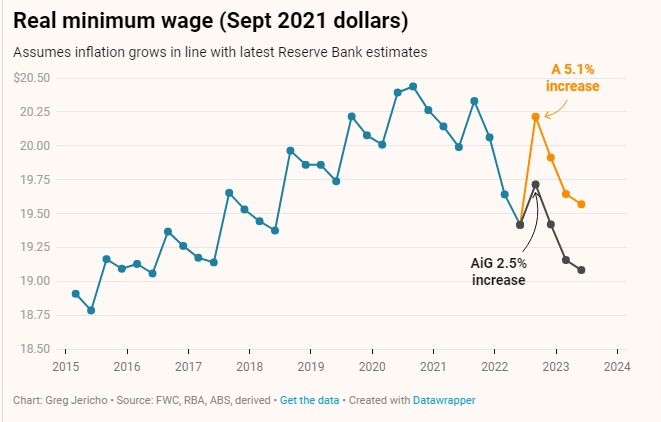

Labour market policy director, Greg Jericho, in his column in Guardian Australia, however notes that wages should grow faster than inflation, and so long as real wages are not outpacing productivity growth then such rises are not exerting any inflationary pressure. He also shows that given the recent estimates for inflation by the Reserve Bank, a 5.1% increase would not be enough to prevent the minimum wage falling in real terms over the next financial year.

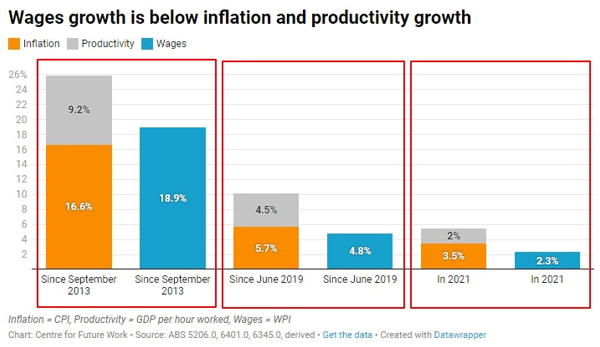

The problem is not that wages have been fuelling inflation, but that for the past 20 years real wages have risen slower than productivity.

We need to change the debate from a reflex that assumes low wages is the ideal to realising that given workers are the economy they should be rewarded fairly for their efforts and improvements in productivity.

You cannot say the economy is healthy if real wages are falling, and most certainly not if the lowest paid in Australia are seeing their living standards decline.

The post Real wages should rise – anything else means declining living standards appeared first on The Australia Institute's Centre for Future Work.

Today the opposition leader, Anthony Albanese was asked about wages in the following exchange:

Journalist: “You said that you don’t want people to go backwards. Does that mean that you would support a wage hike of 5.1% just to keep up with inflation?

Anthony Albanese: “Absolutely”.

Any other response would be to suggest that real wages – and thus people’s ability to purchase goods and services with the money they earn – should decline.

The suggestion that wages rising in line with inflation or even marginally above inflation will increase inflation in a “return to the 1970s” wage spiral ignores basic economics and the advice of the Treasury department.

Real wages should rise – and unless they are outpacing productivity there is no case to be made that they are driving inflation.

This very point was made in February by the Secretary of the Treasury, Steven Kennedy when he noted

“if we can achieve productivity growth of 1.5 per cent, then nominal wages [assuming inflation of 2.5 per cent] can grow at four per cent and put no pressure on inflation”[i].

The problem is not that wages are growing too fast, but that over the past 3 years they have not kept pace with inflation and productivity growth.

From June 2019 to the end of 2021 inflation has increased 5.7% and productivity has grown by 4.5%. And yet rather than wages growth being equal to the sum of those two measures, nominal wages in that period increased just 4.8%, and real wages have fallen 0.8%. Real wages have thus declined, while real labour productivity increased.

The evidence is clear that wages did not cause the current surge in inflation. There is no reason to believe that suppressing wages will cause inflation to moderate. Asking workers to accept a permanent reduction in their real living standards to fight inflation that they did not cause is neither fair nor economically sensible.

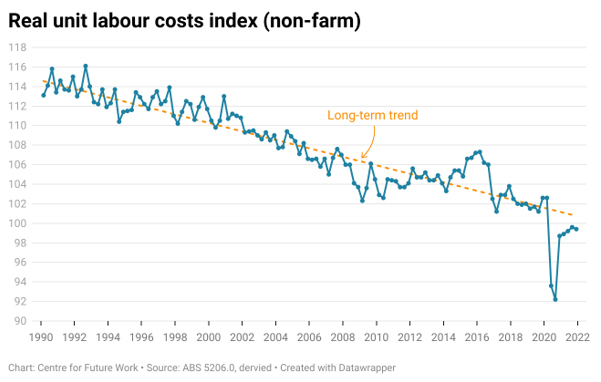

The Reserve Bank has rightly suggested that it will keep an eye on labour costs, however it should be noted that in the 12 months to March while the Consumer Price Index grew 5.1%, the Producer Price Index, which measures the inflation of input costs, rose 4.9%, and nominal unit labour costs grew just 4.0%. This confirms that inflation is not being driven by labour costs.

Moreover, Non-farm, Real Unit Labour Costs are now 3.1% below their pre-pandemic level of December 2019.

That decline is even faster than the long-term trend.

A fall in real wages will only continue the transfer of national income from workers to corporate profits – something which also occurred when inflation was falling. Workers were told then to accept lower wages growth (and also public-sector wage caps) because inflation was low. Now they are being told to accept lower wages because inflation is high – and for no fault of their own.

[i] Economics Legislation Committee, 16 February 2022.

The post Why commentary that wages growing in line with inflation will drive up inflation is completely misguided appeared first on The Australia Institute's Centre for Future Work.

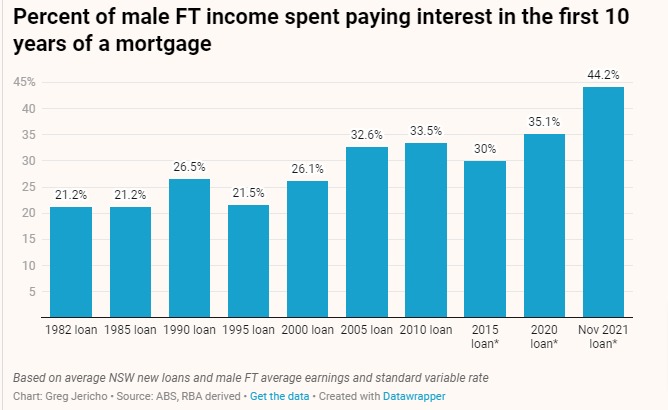

But that is about to change.

The signal that interest rates are going to rise by possibly 2.5% points over the next 18 months means that for new mortgage holders the cost of repaying a mortgage is going to be harder than ever before – harder even than when interest rates hit 17% in 1990.

It is a hit that will only exacerbate standard of living problems as wages will struggle to keep up with the rising cost of of holding a mortgage – especially given the belief that wage rises need to be contained below inflation rises continues in economic debate.

The post Rate rises are going to cause a housing affordability crunch appeared first on The Australia Institute's Centre for Future Work.

Labour market policy director, Greg Jericho, notes in his column in Guardian Australia that even if wages have increased by 2.5% in the next release (up from 2.3% in the 12 months to December) real wages will have fallen 2.5% in the past 12 months.

That would mean real wages would be back at 2014 levels and barely above where they were when the LNP took office in September 2013.

Worse still for low-income earners, in the past 12 months the prices of non-discretionary items rose 6.6%. For those whose income goes more towards paying essential bills than does the average household, the pain of these price rises has been much higher. Their real wages have likely fallen by more than 3% in the past 12 months.

This is why any gloating about a recovery from the pandemic must be tempered to consider the reality of workers’ lives. It is not enough to point to lower unemployment if real wages are falling faster than they ever have outside of the introduction of the GST – especially for lower income earners.

That is not a recovery; that is a failure.

With interest rate rises now very much on the way, without wage rises that account for inflation and properly reward for increases in productivity, workers standard of living is set to fall and see them back where they were nearly a decade ago.

The post High inflation means real wages have plummeted appeared first on The Australia Institute's Centre for Future Work.

And yet, as policy director Greg Jericho notes in his column in Guardian Australia, the issue has been virtually ignored in the election campaign thus far – with most focus being on the “costs” of reducing emissions rather than a focus on the need to do so, or that the cost of renewable energy has fallen so far that “maintaining emission-intensive systems may, in some regions and sectors, be more expensive than transitioning to low emission systems”.

There need to be a focus on the jobs in a low-emissions economy rather than a belief that Australia can keep avoiding the reality of climate change.

The post The election campaign needs to tackle climate change appeared first on The Australia Institute's Centre for Future Work.

Taking this perspective to task in a piece for The New Daily, Jim Stanford and Mark Dean discuss how a much broader range of forms of insecure work face many workers in Australia today, with the issue not getting any better. This is not even a trend created by unavoidable conditions created by the pandemic; it has rather been a deliberate outcome of the federal government’s labour market policies. Simply pretending it isn’t an issue won’t make it go away; nor will it provide us with sustainable solutions to the precarious situation that will keep facing more and more workers until the problem of insecure work is adequately addressed

The post We (still) need to talk about insecure work appeared first on The Australia Institute's Centre for Future Work.

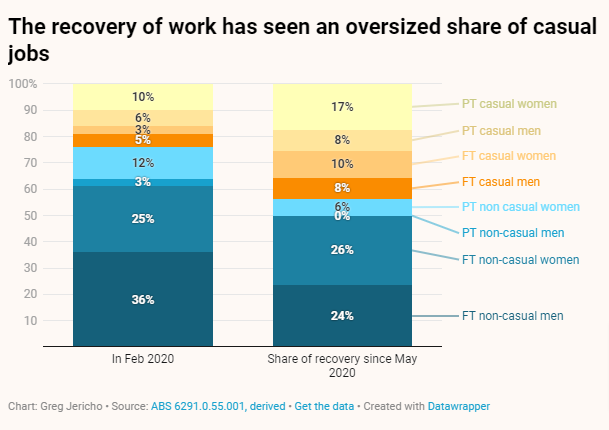

Labour market and fiscal policy director, Greg Jericho writes in his Guardian Australia column that the recovery from the depths of the pandemic has overwhelmingly been on the backs of casual workers. It also has seen a large increase in the gap between people on JobSeeker and the number of unemployed. The rise of low paying, insecure work that has helped bolster the employment figures has also meant people who are working but still earning less than enough to keep out of poverty is remaining high.

The post The election campaign needs to be more than a quiz show appeared first on The Australia Institute's Centre for Future Work.

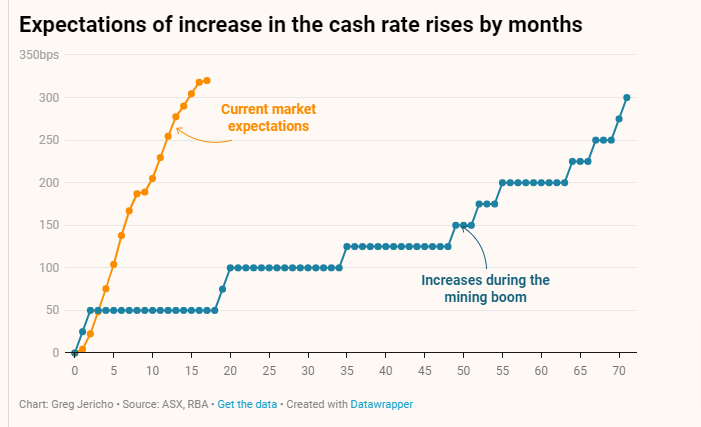

But while that may have been a neutral rate in the past, the Centre’s Fiscal and Labour Market Policy Director Greg Jericho, notes in his column in Guardian Australia, recent surges in house prices means such a rise would place an extreme burdon on mortgage payers – one not conducive to an economy still in recovery.

It took nearly 6 years during the mining boom for the RBA to raise the cash rate by 300 basis points; currently the market anticipates the same rise occurring in 17 months.

That would massively limit economic growth for little purpose at a time when wage rises remains below inflation, and rather unlikely to occur given the Reserve Bank’s recent hesitancy to slow the economy until real wage again start rising.

The post House prices means interest rates do not need to rise much to inflict great costs appeared first on The Australia Institute's Centre for Future Work.