Labour market and fiscal policy director, Greg Jericho writes in Guardian Australia that the rising level of inflation, which combined with low wages growth has led to massive falls in real wages, has many Australians wondering if increasing interest rates is going bring the economy to a halt.

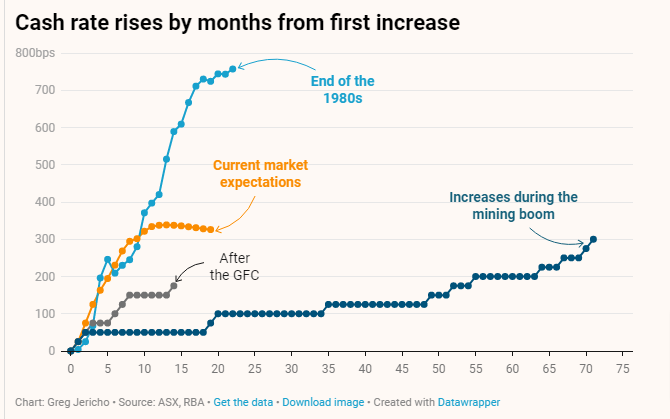

He writes that for now a recession is unlikely, but the risks remain. Previous periods of sharply increasing rates have been followed by rising unemployment, and the current market expectations for the cash rate rising above 3.5% within a year would certainly create a massive brake on the economy.

The story from overseas is also worrying, with the United States battling even higher inflation than Australia and suggestions that the market is already pricing in a recession.

It all highlights that while today’s labour force figures are on the surface very promising, they also show just how affected the economy continues to be by the pandemic. Nearly 300,000 employed in June worked zero hours because of sickness or injury – well over double the usual amount.

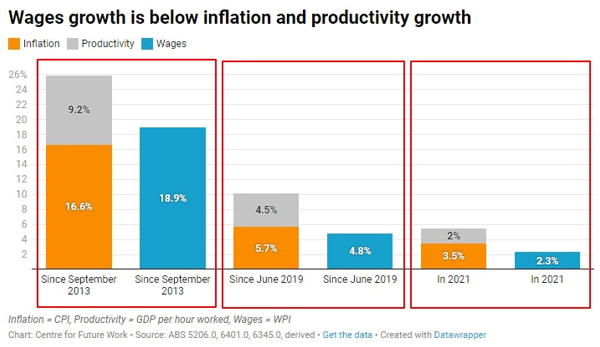

The nearly 50-year low unemployment rates are also failing to lead to wages growth anywhere near what would have been expected in previous years, let alone at a level that is keeping up with inflation.

While inflationary pressure do remain, the risk that the Reserve Bank will raise rates too high and too fast remains very much in place – especially given the lack of wages growth.

The post Will “curing” inflation cause a recession? appeared first on The Australia Institute's Centre for Future Work.