But as Labour Market and Fiscal Policy Director, Greg Jericho, notes in his Guardian Australia column, the latest monthly inflation figures out yesterday suggest that maybe the peak could be lower than anticipated.

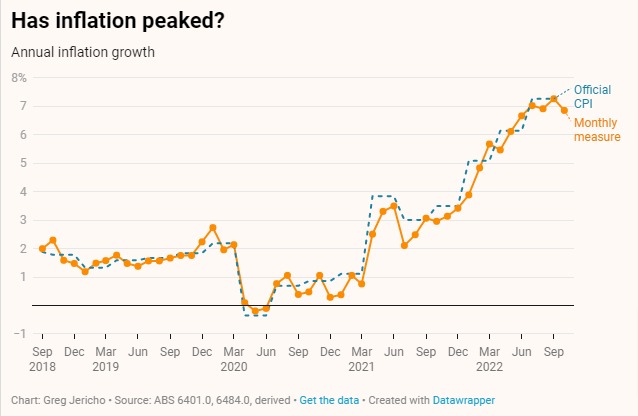

While the monthly figures can be a little erratic, they do closely align with the quarterly “official” CPI figures and in October the ABS estimates that annual inflation growth fell from 7.3% to 6.9%. Better still this makes 4 months in a row where inflation has remained around 7%, rather than increasing quickly as it has since the middle of last year.

Combined with the latest Retail Trade figures released this week which showed the dollar amount spent in the shops fell in October, and the volume of spending falling even faster, there are solid signs that the interest rate rises are having an impact.

This means the Reserve Bank needs to be very cautious as much of the impact of the rate rises from September October and November has yet to flow through into the data. And because the rates of existing mortgages take longer to rise than do rates for new home loans this also means that even were the RBA to halt rate rises, for most mortgage holders rates will still be about to rise over the next few months.

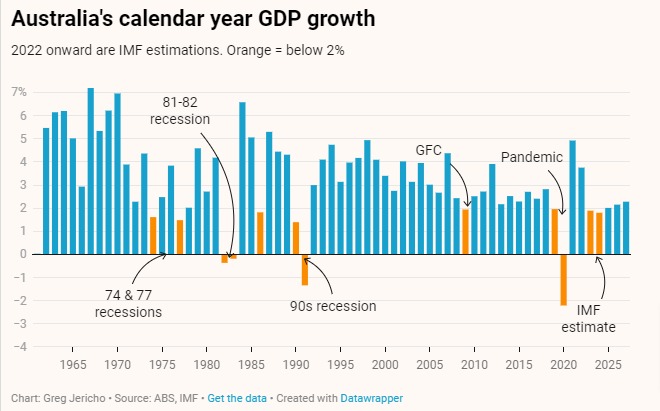

The IMF, OECD, Treasury and the RBA itself all forecast a sharp slowing of Australia’s economy next year and into 2024. The rationale has been that this is the cost of needing to reduce inflation, but the central bank needs to be very careful that it does not commit overkill. With the economy and consumer spending already slowing, and inflation showing some good signs that growth is no longer increasing at a rapid rate, the RBA should strongly consider not increasing the rate next week in its final board meeting of the year.

The post The Reserve Bank needs to watch that it doesn’t push the economy off a cliff appeared first on The Australia Institute's Centre for Future Work.