Over the past year, the main driver of inflation has been house prices accounting for a quarter of the 7.3% rise in the CPI. And yet we know that house price growth is now either slowing dramatically or even falling in some areas. The RBA has also noted that commodity prices are falling and supply-side issues are being dealt with and that these aspects, which are not influenced by interest rates, will reduce inflation next year.

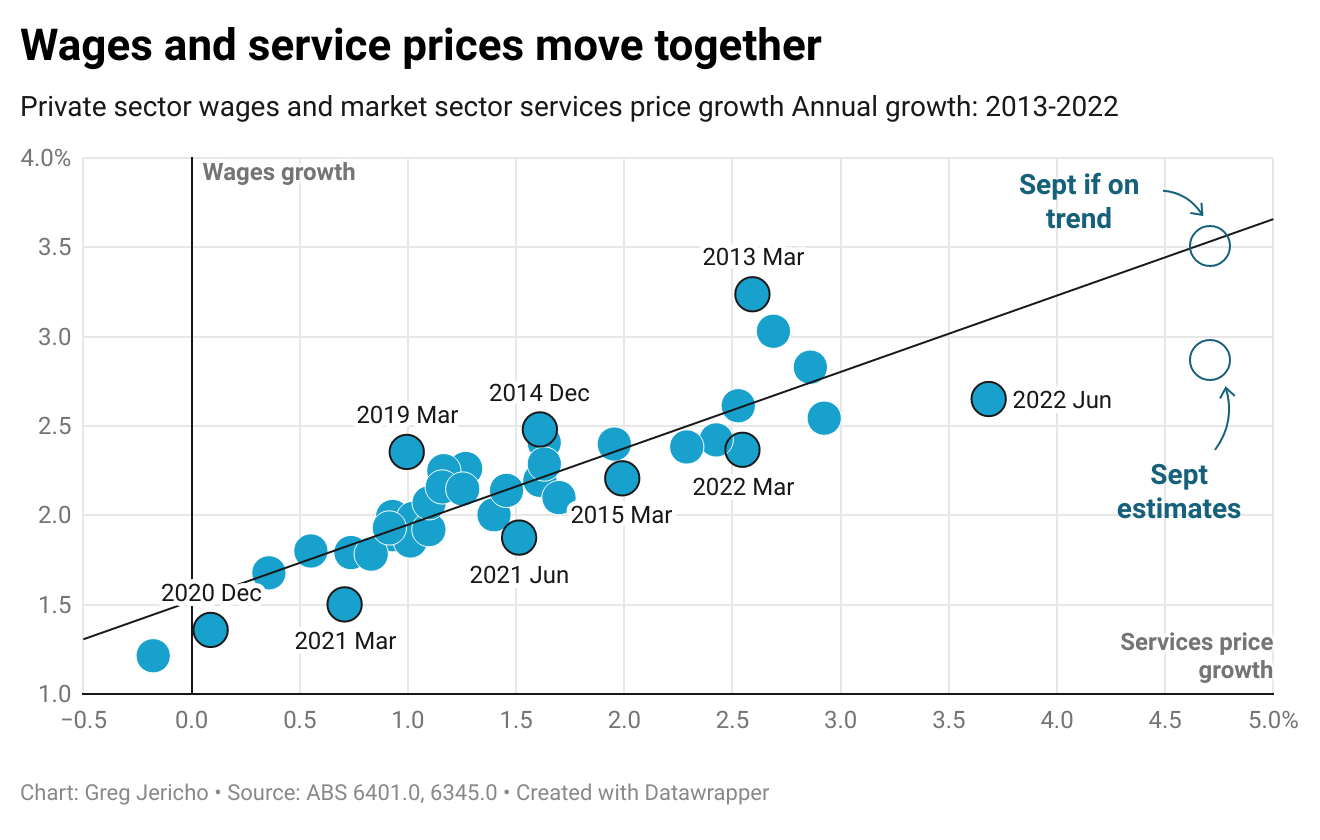

At the same time, the Reserve Bank continues to sound warnings of a wage-price spiral despite any evidence of such a thing occurring. Indeed the latest CPI figures show that overwhelmingly inflation is driven by the price rises of goods rather than services. This is important because service prices and wages are strongly linked.

More rate rises will certainly continue to reduce demand in the economy as the cost of servicing a mortgage rises. But to what end? The main factors driving inflation are easing, wages have not risen above 3% yet, let alone to a rate anywhere near inflation.

Even if wages were to rise in line with the historical link with service prices, in September they would have risen 3.5% – a level very much consistent with inflation growth of between 2% and 3%. And yet we know that wages are unlikely to rise that fast. The most recent estimates have it closer to 2.8%.

The great risk now is that further rate rises will only hurt the economy for little gain and see wages growth stunted before they even get to a level that would see real wages rising.

The post Would further interest rate rises do more harm than good? appeared first on The Australia Institute's Centre for Future Work.